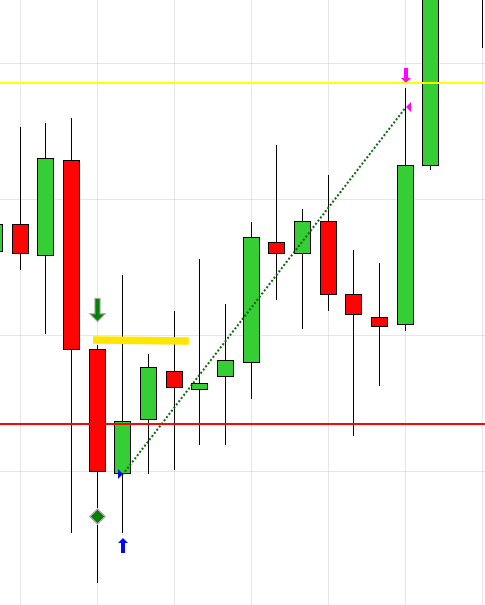

I have some issues with the strategy below. The current thing i am trying to work out is where it enters. The strategy is a 5 min ORB that tracks the orb then signals on a close outside the ORB using that candle with the first close outside candle as the range for the entries. Entering a long on the break of the high and a short with a break of the low. It should enter at the H/L of the signal candle but its seems to be entering at the 5 min close. I believe I have it configured to evaluate by the tick so im not sure why its only entering on the close.

#region Using declarations

using System;

using System.Collections.Generic;

using System.ComponentModel;

using System.ComponentModel.DataAnnotations;

using System.Linq;

using System.Text;

using System.Threading.Tasks;

using System.Windows;

using System.Windows.Input;

using System.Windows.Media;

using System.Xml.Serialization;

using NinjaTrader.Cbi;

using NinjaTrader.Gui;

using NinjaTrader.Gui.Chart;

using NinjaTrader.Gui.SuperDom;

using NinjaTrader.Gui.Tools;

using NinjaTrader.Data;

using NinjaTrader.NinjaScript;

using NinjaTrader.Core.FloatingPoint;

using NinjaTrader.NinjaScript.Indicators;

using NinjaTrader.NinjaScript.DrawingTools;

#endregion

//This namespace holds Strategies in this folder and is required. Do not change it.

namespace NinjaTrader.NinjaScript.Strategies

{

public class FiveBreak : Strategy

{

private DateTime lastExitSessionTime = Core.Globals.MinDate;

private TimeSpan tradingStartTime = new TimeSpan(7, 30, 0); // 9:30 AM

private TimeSpan tradingEndTime = new TimeSpan(15, 59, 0);

private TimeSpan tradingStartEndTime = new TimeSpan(8, 30, 0);

private TimeSpan endTradingTime = new TimeSpan(14, 0, 0); // 9:30 AM

private TimeSpan orbStartTime = new TimeSpan(7, 30, 0); // 9:30 AM

private TimeSpan orbEndTime = new TimeSpan(7, 35, 0);

private double orbRangeHigh;

private double orbRangeLow;

private double orbRangeMid;

private bool ordersPlaced = false;

private bool lastBarWasSignal = false;

private bool hasTraded = false;

private double longOrderPrice = 0;

private double shortOrderPrice = 0;

private double signalBarHigh = 0;

private double signalBarLow = 0;

private string longOrder = "LongBreakout";

private string shortOrder = "ShortBreakdown";

private int signalBarNum = 0;

protected override void OnStateChange()

{

if (State == State.SetDefaults)

{

Description = @"Enter the description for your new custom Strategy here.";

Name = "FiveBreak";

Calculate = Calculate.OnEachTick;

EntriesPerDirection = 1;

EntryHandling = EntryHandling.UniqueEntries;

IsExitOnSessionCloseStrategy = true;

ExitOnSessionCloseSeconds = 30;

IsFillLimitOnTouch = false;

MaximumBarsLookBack = MaximumBarsLookBack.TwoHundredFiftySix;

OrderFillResolution = OrderFillResolution.Standard;

Slippage = 0;

StartBehavior = StartBehavior.WaitUntilFlat;

TimeInForce = TimeInForce.Gtc;

TraceOrders = false;

RealtimeErrorHandling = RealtimeErrorHandling.StopCancelClose;

StopTargetHandling = StopTargetHandling.PerEntryExecution;

BarsRequiredToTrade = 20;

// Disable this property for performance gains in Strategy Analyzer optimizations

// See the Help Guide for additional information

IsInstantiatedOnEachOptimizationIteration = true;

IsTickReplay = true; // This must also be enabled on the chart or strategy analyzer

}

}

protected override void OnBarUpdate()

{

if (CurrentBar < 25 )

{

return;

}

// Only act on the last bar of the session AND only once

if (Bars.IsLastBarOfSession && Times[0][0].Date > lastExitSessionTime.Date)

{

if (Position.MarketPosition != MarketPosition.Flat)

{

ExitLong(); // Will only affect open longs

ExitShort(); // Will only affect open shorts

}

// Mark this session as already processed

lastExitSessionTime = Times[0][0];

}

// Get ORB H/Ls

if ( Time[0].TimeOfDay >= orbStartTime && Time[0].TimeOfDay <= orbEndTime)

{

if (Time[0].TimeOfDay == orbStartTime)

{

orbRangeHigh = High[0];

orbRangeLow = Low[0];

//fiveHasClosedAbove = false;

//fiveHasClosedBelow = false;

ordersPlaced = false;

hasTraded = false;

}

if (High[0] > orbRangeHigh)

{

orbRangeHigh = High[0];

}

if (Low[0] < orbRangeLow)

{

orbRangeLow = Low[0];

}

}

// Print lines For ORB

if ( Time[0].TimeOfDay >= orbStartTime)

{

orbRangeMid = ((orbRangeHigh - orbRangeLow) / 2) + orbRangeLow;

Draw.Line(this, "ORBHigh" + CurrentBar, false, 1, orbRangeHigh, 0, orbRangeHigh, Brushes.Green, DashStyleHelper.Solid, 2);

Draw.Line(this, "ORBLow" + CurrentBar, false, 1, orbRangeLow, 0, orbRangeLow, Brushes.Red, DashStyleHelper.Solid, 2);

Draw.Line(this, "ORBMid" + CurrentBar, false, 1, orbRangeMid, 0, orbRangeMid, Brushes.Yellow, DashStyleHelper.Solid, 2);

}

// Look for close outside ORB

if (Time[0].TimeOfDay >= orbEndTime)

{

// Break High of range

if (IsFirstTickOfBar && Close[1] > orbRangeHigh && Close[2] < orbRangeHigh && !lastBarWasSignal)

{

Draw.ArrowUp(this, "UpperBreak " + CurrentBar + Time, false, 1, Low[1] - (TickSize * 10), Brushes.Green);

signalBarNum = CurrentBar;

signalBarHigh = High[1];

signalBarLow = Low[1];

lastBarWasSignal = true;

}

if (IsFirstTickOfBar && Close[1] < orbRangeLow && Close[2] > orbRangeLow && !lastBarWasSignal)

{

Draw.ArrowDown(this, "UpperBreak " + CurrentBar + Time, false, 1, High[1] + (TickSize * 10), Brushes.Green);

signalBarNum = CurrentBar;

signalBarHigh = High[1];

signalBarLow = Low[1];

lastBarWasSignal = true;

}

if (BarsInProgress != 0)

return;

//CurrentBar - signalBarNum > 0

if (Time[0].TimeOfDay >= orbEndTime && Position.MarketPosition == MarketPosition.Flat && lastBarWasSignal ) // && CurrentBar - signalBarNum > 0 && CurrentBar - signalBarNum < 2)

{

// Test for close outside ORB

if (Close[0] > signalBarHigh )

{

Draw.Diamond(this, "EnterLongHere" + CurrentBar + Time, false, 1, Low[0] - TickSize * 10, Brushes.Green);

SetUpLongOrders(1, 1, signalBarHigh, signalBarLow);

lastBarWasSignal = false;

}

if (Close[0] < signalBarLow )

{

Draw.Diamond(this, "EnterShortHere" + CurrentBar + Time, false, 0, High[0] + TickSize * 10, Brushes.Red);

SetUpShortOrders(1, 1, signalBarHigh, signalBarLow);

lastBarWasSignal = false;

}

}

}

}

private void SetUpLongOrders(int orderMultiplier, int orderTypes, double highOrderPrice, double lowOrderPrice)

{

double longSL = lowOrderPrice;

double slRange = highOrderPrice - lowOrderPrice;

double targetMultiplier = 1;

double longTarget = (highOrderPrice + (slRange * targetMultiplier));

EnterLong(1, longOrder);

SetStopLoss(longOrder, CalculationMode.Price, shortOrderPrice, false);

SetProfitTarget(longOrder, CalculationMode.Price, longTarget);

ordersPlaced = true;

lastBarWasSignal = false;

}

private void SetUpShortOrders(int orderMultiplier, int orderTypes, double highOrderPrice, double lowOrderPrice)

{

double slRange = highOrderPrice - lowOrderPrice;

double targetMultiplier = 1;

double shortTarget = (lowOrderPrice - (slRange * targetMultiplier));

EnterShort( 1, shortOrder);

SetStopLoss(shortOrder, CalculationMode.Price, longOrderPrice, false);

SetProfitTarget(shortOrder, CalculationMode.Price, shortTarget);

ordersPlaced = true;

lastBarWasSignal = false;

}

}

}