Are there any experts that have profitable automated strategies that will go over others strategies and look for improvements?

I have what I would call excellent numbers but I’m afraid to take them live. I have taken others live with disastrous results. I’ve learned from mistakes, but still fear going live. If there’s a resource for hire, would look it (them) over and say, yeah, this is very promising, or looks good but you need to add this, tweak that, it’s doomed to fail, etc. I’d feel much better.

And no, I’m not just gonna trust any dipstick with my work. I’d have to have someone that’s done it before and has references, etc. I don’t want my work stolen, not sure how to protect against that other than check references, credentials, and a hell of a lotta trust!

Thanks for any feedback, only qualified persons apply.

I am new to ninjatrader, but I have also heard that if strategy is only putting market orders, strategy analyzer can be more accurate than market replay with a secondary tick data series, the intra bar simulation of market replay is horrible.

I only trust the live feed, no one is gonna provide good historical data for free.

That is totally correct, no reviews mean anything if forward testing does not have good results, and if forward testing is having good results, what is the need of a review…as far as ideas of improvement are concerned everyone has those ideas…ideas dont make money, it is the implementation and execution that matters, if you are not confident about a fully automated strategy what you need to do is get a good trader to partner with you and ask the good trader who reads the market well to combine his know how with the strategy. Fututes market you are either going to make big profit or loose everything, there has never been any need for a fully automated strategy, the cost of time spent in sitting with the strategy and controlling it is minimal compared to the cost of money that is at stake, so one would never want to leave the computer unattended even with the most robust strategy in place.

Having said that I am myself designing my workflow such that it should be enough to just spend 20 hours over the weekend to keep the system running efficiently.

Thank you Bobby for a useful reply. Your number one, Strategy Analyzer has pretty amazing numbers. Number 2, I haven’t figured out how to use market replay. Tried it a couple times and wasn’t sure I was using it right. Number 3, yes I’ve been getting good results live trading sim ever since I fixed big drawdown days to stop the bleeding on what are typically big range consolidation days that happen to be in my trigger range.

My thought for this post was as follows. I’m not the most intelligent or experienced guy doing this. Even well respected Drs. and professors have their pre-published work “peer reviewed”. Why? Other sets of eyes and experience levels can have reinforcing and objective comments to improve integrity of the end product. I guess if I thought I were the smartest, and no one could possibly have anything constructive to add, I wouldn’t seek other comments and opinions. I’m not an island and I’m not a self absorbed egotistical.

Your order of importance is helpful. I may try the market replay again. It seems Ninja’s tutorials, if they have anything are scattered like the wind. And many times a search leads you to the programming help side of it. That’s no help. Strategy builder was made for folks who don’t have any desire to learn programming.

OK, too long winded, thanks again for the useful feedback.

Over the past two years I’ve developed a separate, fully private analytics application that does exactly what you’re describing.

In short: strategies are run in NinjaTrader using Market Replay (the closest proxy to live execution), with a structured feed captured during execution. That data is then analysed in Python to statistically identify when a strategy should trade and when it should not. From this, I generate objective “gates” or rules based purely on observed performance characteristics, not intuition.

I’ve spent a significant amount of time validating this workflow specifically to address the gap between strong backtest numbers and the anxiety of live deployment. In multiple cases, the output has materially improved stability and reduced failure modes that only become visible when you analyse trades at scale.

This is not a public platform, and I’m very cautious around IP and trust for the same reasons you’ve outlined. I’m not offering to take anyone’s code or signals. I’m open to a discussion about whether the process could be useful in your case, and I can show anonymised examples of the type of improvements it produces.

This is really interesting, just to dig in a bit what exactly does your tool analyse in the sense what data…if I as an algorithmic trader provide to you the list of trades my strategy made and the results they got say in the last 6 months, is that all your tool needs to give extra parameters to the strategy to add to their rules in order to reduce the losers…my strategy never places a trade with stop loss greater than 70 ticks, so drawdown is not really a concern in this case, its either win or loose scenario.

Not trying to pry into your software but just trying to understand where it fits in the workflow and what value does it bring…because it sounds like it is not tied specifically with your strategy but is more of a generic tool.

That’s a fair question, and I’ll keep this at the right level.

Short answer: a list of trades and outcomes alone is not sufficient for the work I’m describing.

Trade results (wins/losses, PnL, stop size, etc.) tell you what happened, but not why it happened. Many strategies that appear stable on trade-level statistics still fail live because the failure modes sit upstream of the entry decision, not purely in exit sizing.

At a high level, the analysis looks at context around each trade, not just the trade outcome. That context is strategy-specific, which is why this isn’t a generic “upload trades → get better rules” tool.

A few clarifications that may help:

This is not primarily about optimising stops or targets

Your point about capped stop size is valid, but fixed risk per trade only bounds individual losses. Most meaningful drawdowns come from clusters of correlated losses rather than oversized stops. While aspects of the analysis can inform risk parameters such as stops or targets, those are secondary outcomes rather than the core purpose.

The value is in identifying when a strategy should not participate

The focus is on identifying repeatable conditions under which a strategy’s edge degrades or inverts. The output is not abstract “rules to reduce losers”, but evidence-backed guidance on when entries should be suppressed, even though the underlying strategy logic remains unchanged.

It is strategy-agnostic in principle, but not plug-and-play in practice

The process does not depend on my own strategies, but it does depend on understanding how your strategy behaves. That’s why trade logs alone are insufficient, and why this is done as a private, strategy-specific diagnostic rather than a generic tool.

It fits before live deployment, not as a post-hoc fix

The intended use is to reduce uncertainty before going live, particularly in cases where backtests appear strong but confidence is low due to past live failures.

I’m deliberately keeping the mechanics abstract here, but hopefully that clarifies where it fits in the workflow and the type of value it’s designed to provide.

Happy to discuss further one-to-one if it looks relevant.

Definitely very interesting, its a inversion of perspective that could bring great value where the base perspective (the usual one) is when to enter, and then overlay with this perspective when not to enter, && the two conditions and get a valid entry…

The challenge I find is also quantifying the impact of decisions made, when there is so much data so much going on it is so easy to get lost in all this and fall in the cognitive dissonance trap which impedes all manual traders, that I find is the biggest misconception about algo trading, emotions play a huge part in strategy development because it is just so difficult to validate quantify the impact of every decision made at the level of the algorithm.

I will surely love to chat more on this one on one when I am out of my development phase, probably next 4 to 6 months, and I need to have some quality understanding of where I stand before I can present the right questions to you.

Thanks for the thoughtful note, Vipin — you’ve articulated the challenge well.

I agree that quantifying decision impact and avoiding self-reinforcing bias is one of the hardest parts of strategy development, particularly when complexity increases. It sounds like you’re taking a disciplined approach by wanting clarity before drawing conclusions.

Feel free to reach out once you’re further along and have a clearer view of what you’re looking to validate. In the meantime, best of luck with the build phase.

You can possibly, just add logging for your trades. For example, when your strategy enters a trade, include the indicators, parameters and maybe a few previous bars for context. Later on, have an LLM analyze your trades. Personally, I would clone the strategy in Python and play around with it with machine learning models.

Agreed that logging and analysis are a necessary starting point. Where it tends to get tricky is that the challenge usually isn’t collecting more data or replaying the strategy in another language — it’s being able to attribute which decisions materially change outcomes, and under what conditions, without introducing hindsight or confirmation bias.

LLMs and ML models can be useful exploratory tools in that process, but without a disciplined framing they often end up amplifying noise rather than reducing uncertainty. That’s where a lot of people get stuck.

In practice, the harder problem is deciding what not to act on, rather than generating more signals or strategy variants.

If you like an opinion (evaluation) based on nearly 30 years of live experience in developing automated trading systems, feel free to contact me in private.

Sounds pretty interesting…

Could you share some walk-forward testing results (w splitting)?

Does your approach involve engineering extra features beyond the strategy’s own ones?

On walk-forward testing:

I’m careful with the term because it tends to mean different things to different people. There has been a limited live walk-forward period so far, and the live behaviour has remained within tolerance of the historical behaviour the work was derived from (in that window it was slightly better). That said, the live sample is still early and deliberately treated as non-definitive — more as a sanity check that the process isn’t breaking when exposed to real execution.

Internally, most of the validation is done via chronological segmentation and rolling out-of-sample checks rather than a rigid, one-size-fits-all WFA label. The emphasis is on stability across time and conditions, not on “passing” a single formal test.

On feature engineering:

No new entry-generation logic is introduced. The approach does not invent alternative signals or re-express the strategy in another form. What comes out of the process are filters — effectively allow / block conditions — that sit orthogonal to the existing strategy and control participation.

In practice, these are implemented as a standalone, user-configurable gate within the strategy (for example, an “enable / bypass QD gates” switch). This allows the same strategy to run unchanged, with the gating logic either applied or bypassed for validation and comparison. The intent is to isolate the impact of participation control without altering the core entry logic.

The core strategy remains intact; the work is about understanding when its edge is present and when it is compromised, rather than redesigning how entries are generated.

I get the point about live being the ultimate sanity check, but walk-forward is usually demonstrated on historical data. If live is still too short to share, could you provide the historical rolling OOS / walk-forward results?

You’re right that walk-forward validation is typically demonstrated on historical data.

To be precise about where things stand: historical data so far has been used primarily for behavioural discovery and gate design across multiple regimes, rather than for a formalised expanding walk-forward presentation. The validation discipline I’m committing to is an expanding, forward-only walk-forward structure using contiguous quarterly out-of-sample blocks.

In that framework, out-of-sample evidence isn’t a single hold-out or equity curve, but a sequence of independent forward periods, each evaluated against the behaviour it was derived from. Internally, stability is assessed by whether the gates reduce damage during adverse periods and remain neutral during favourable ones, rather than by aggregate return metrics.

The emphasis is on behavioural consistency and failure suppression, not on producing a single historical “proof” curve.

Every time I have excellent numbers I’ve made a mistake. Good systems usually have promising numbers, but rarely excellent. I’d wager your excellent numbers will not hold up in live trading.

There are many ways to get fake backtests on historical data in any trading platform. You can “hack” them essentially if you do something wrong. Another way to hack your systems is inadvertently or intentionally using future data. Even the smallest amount of future information can end up skewing your results to look much better than they should.

So, you are wise to question your systems and seek outside input. It will be worth it to improve your process.

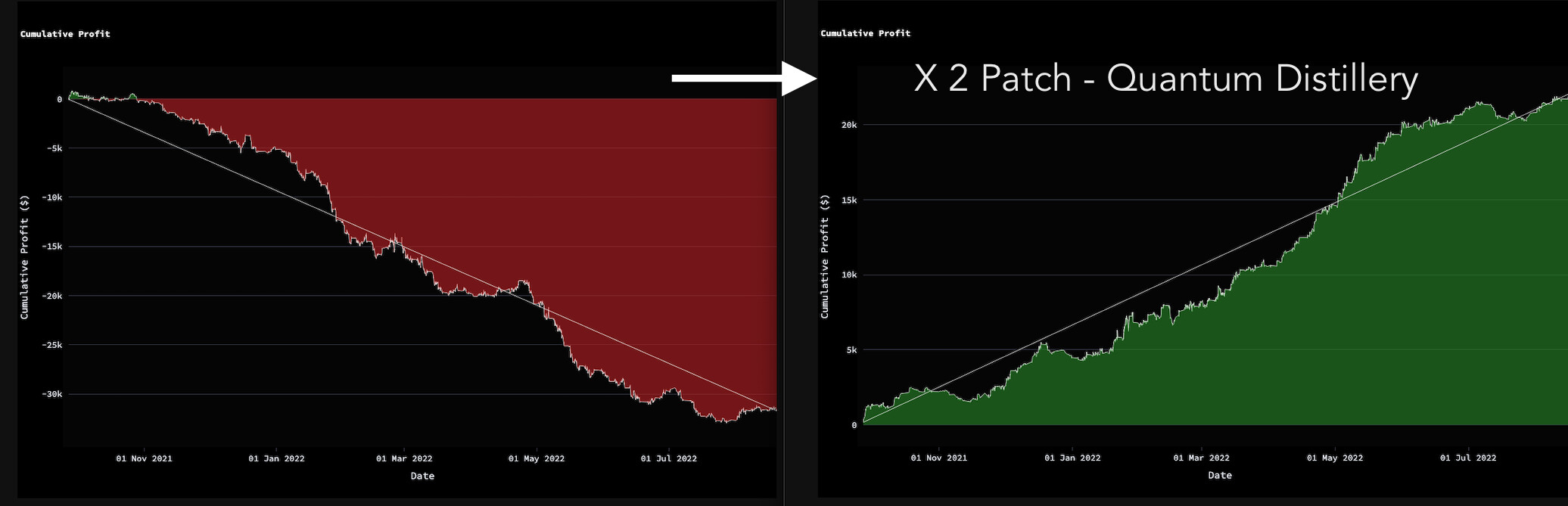

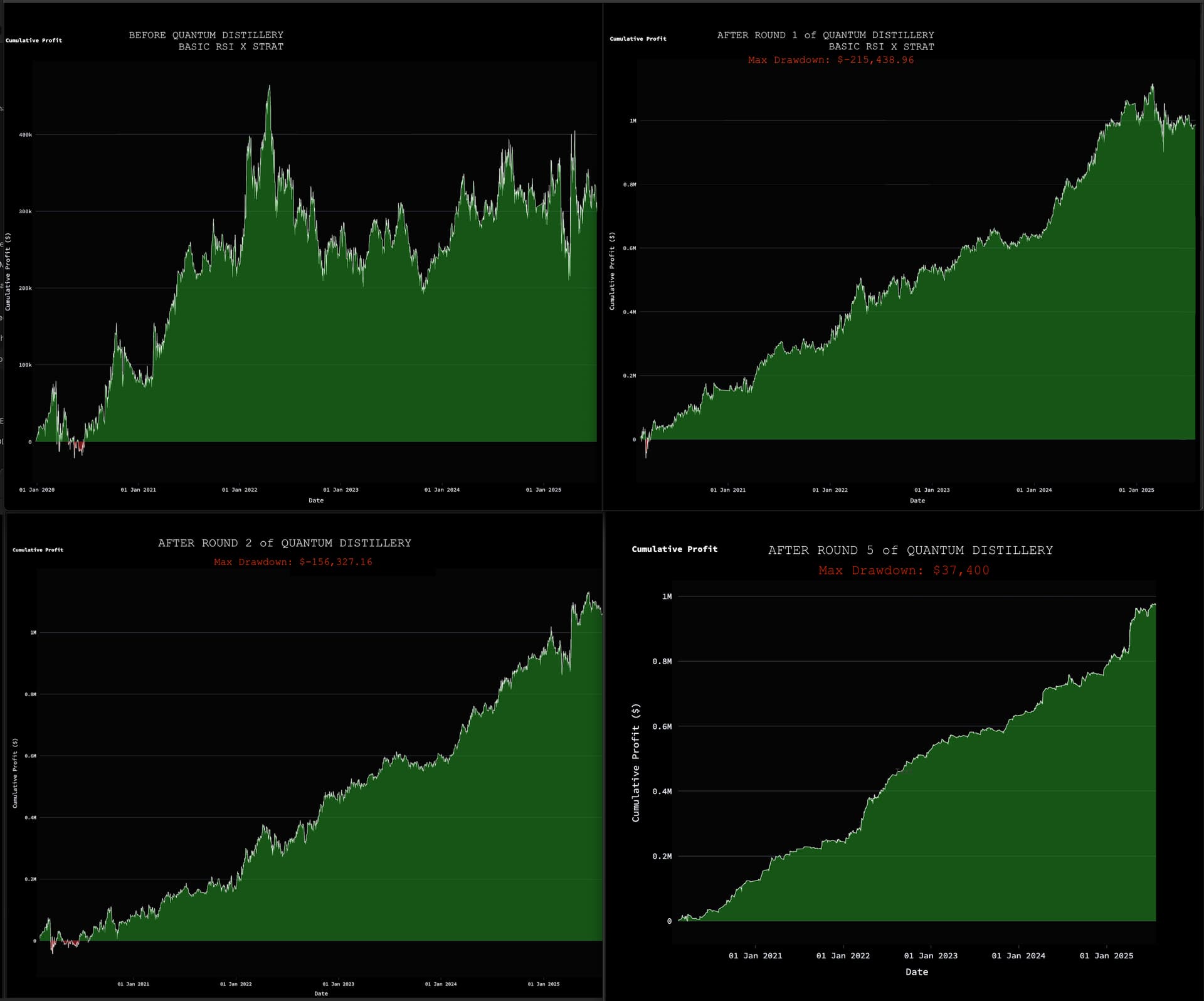

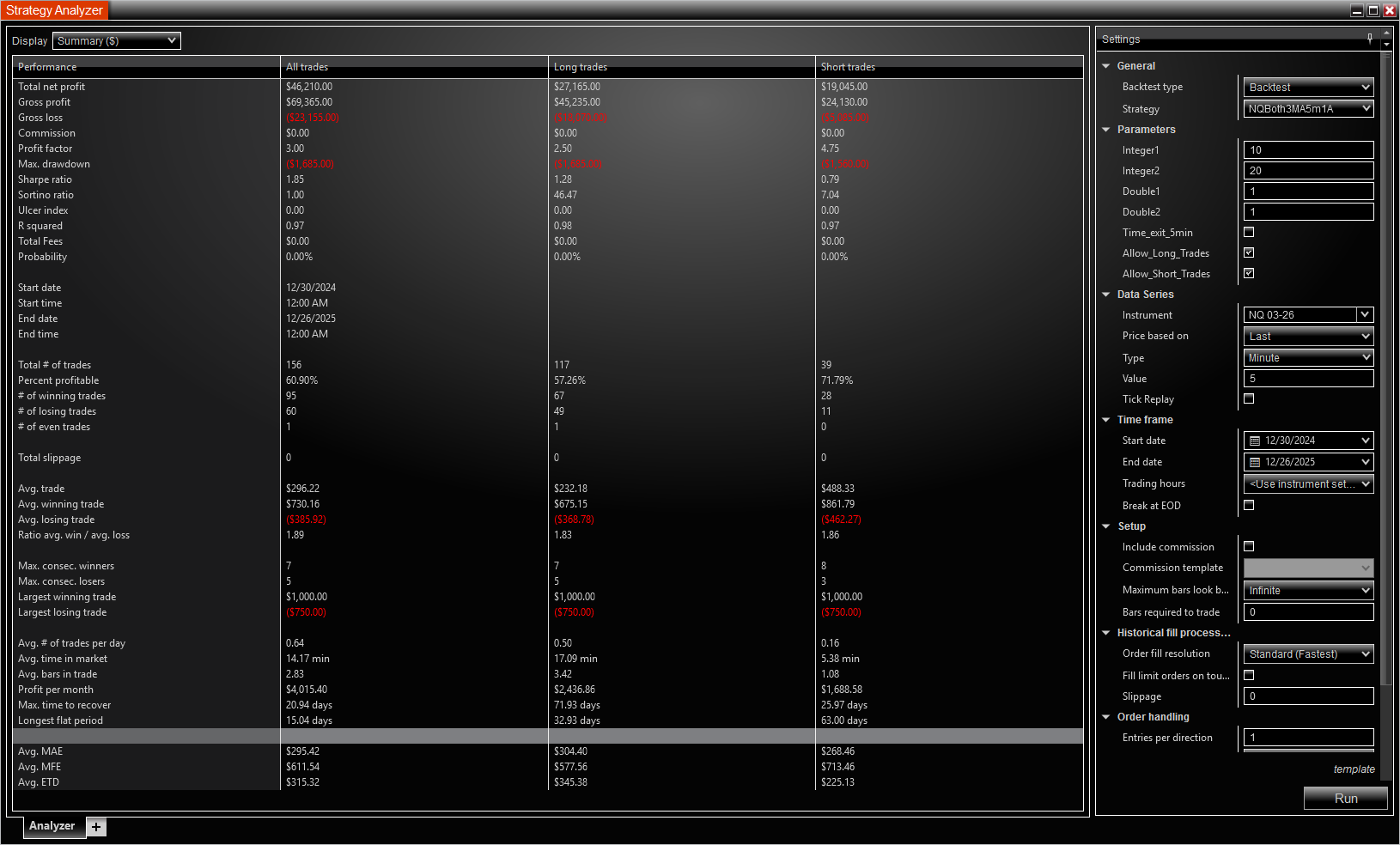

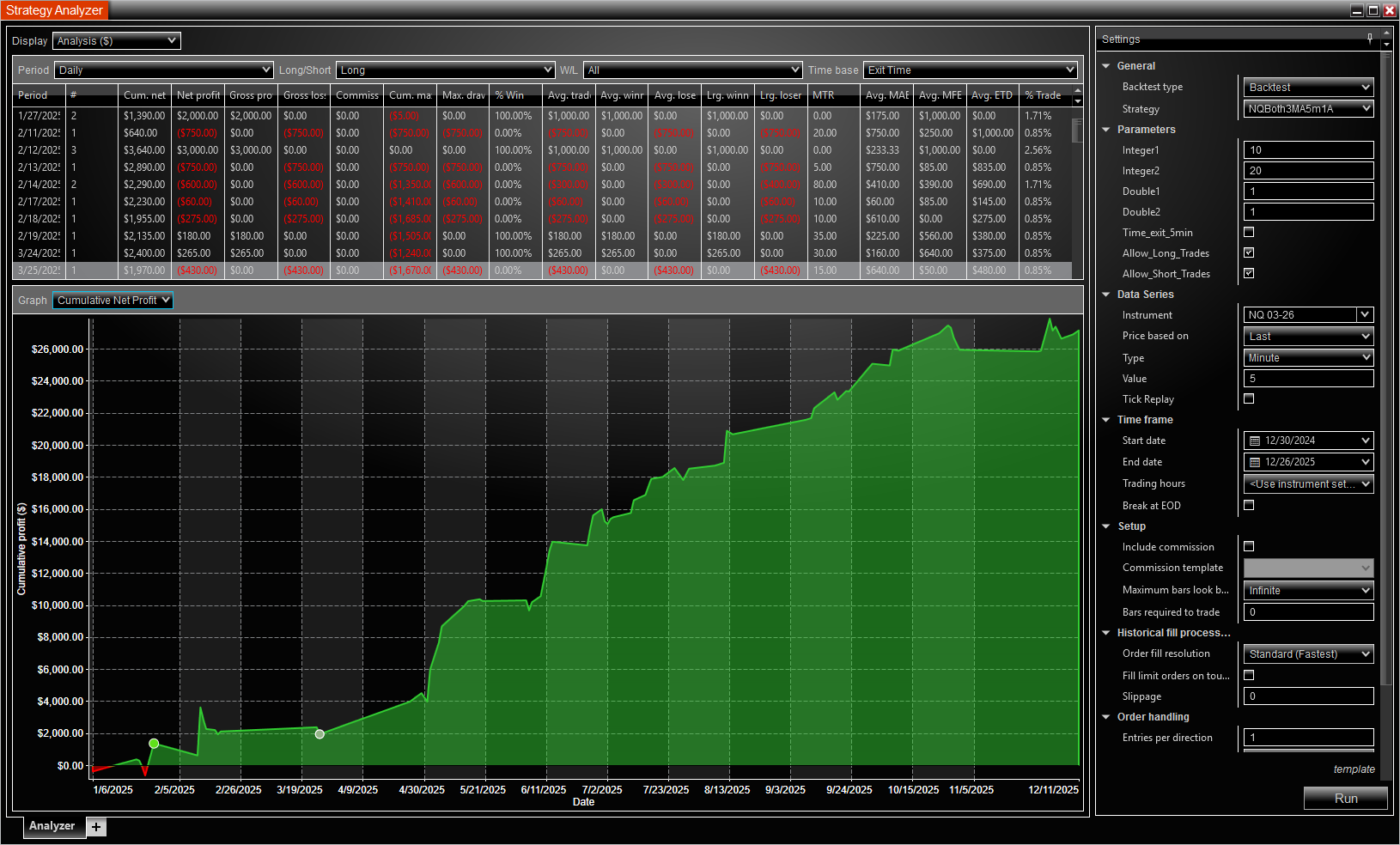

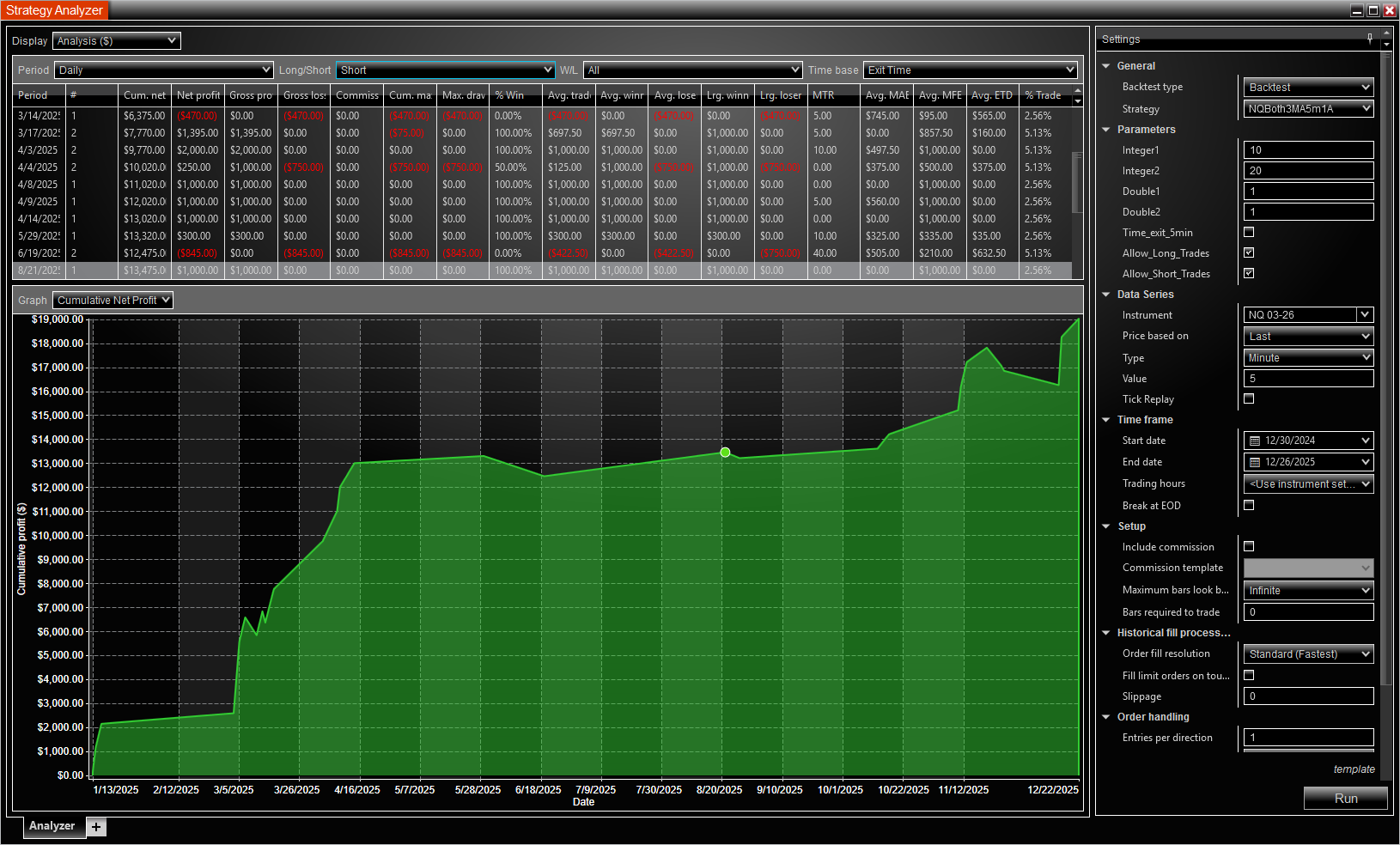

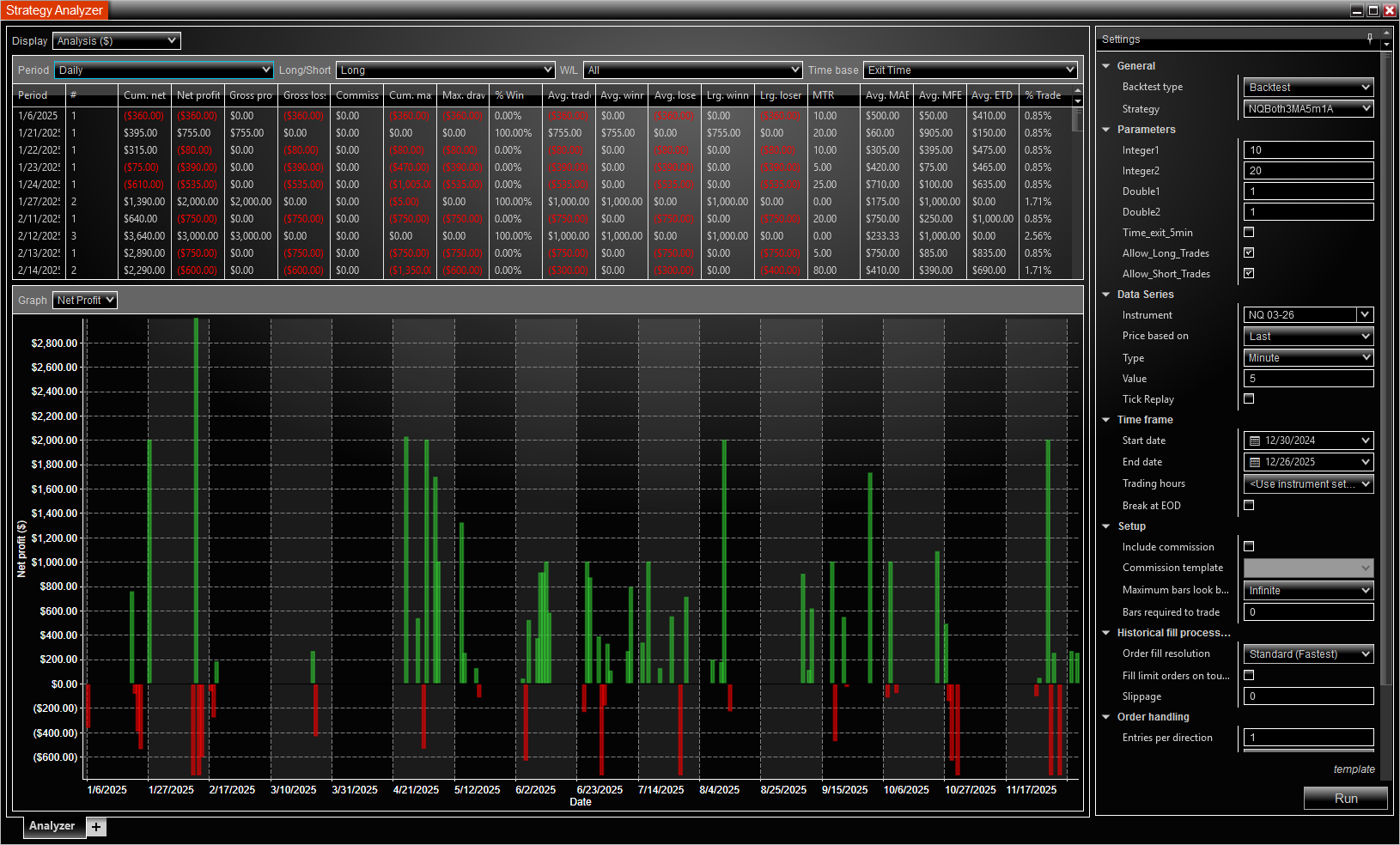

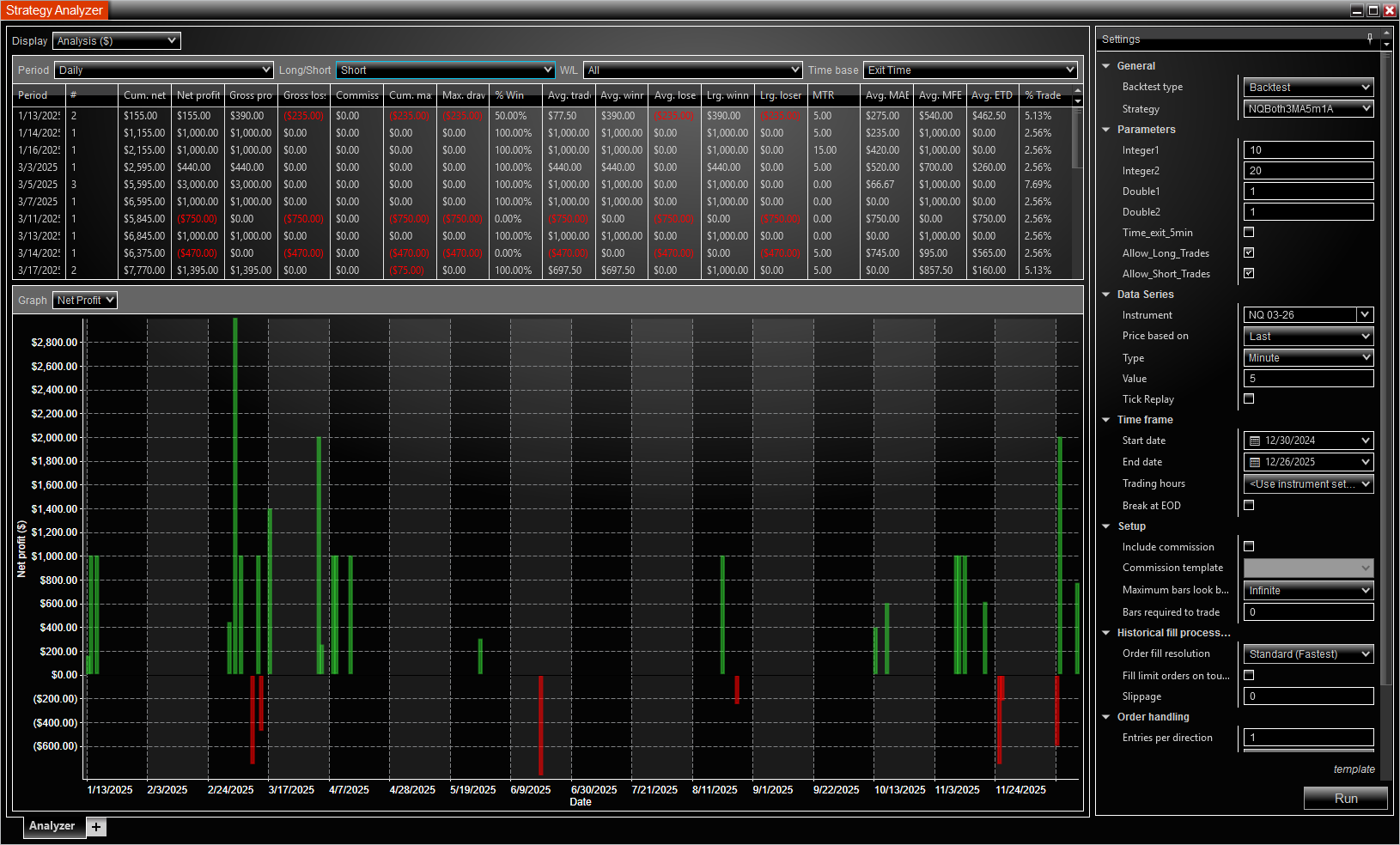

You’re “meat grinder” sounds very interesting. Look at these backtest numbers. They look great, but I’m fearful of going live at this point. I’m running them live SIM and they’re doing OK so far, but not enough trades yet.

Any comments appreciated on these backtests, 5 minute NQ all last year. At this point, would you further “grind” this strategy?

P.S., I’m not familiar using this forum, hence I’ll try and paste pics, thank you for any helpful comments